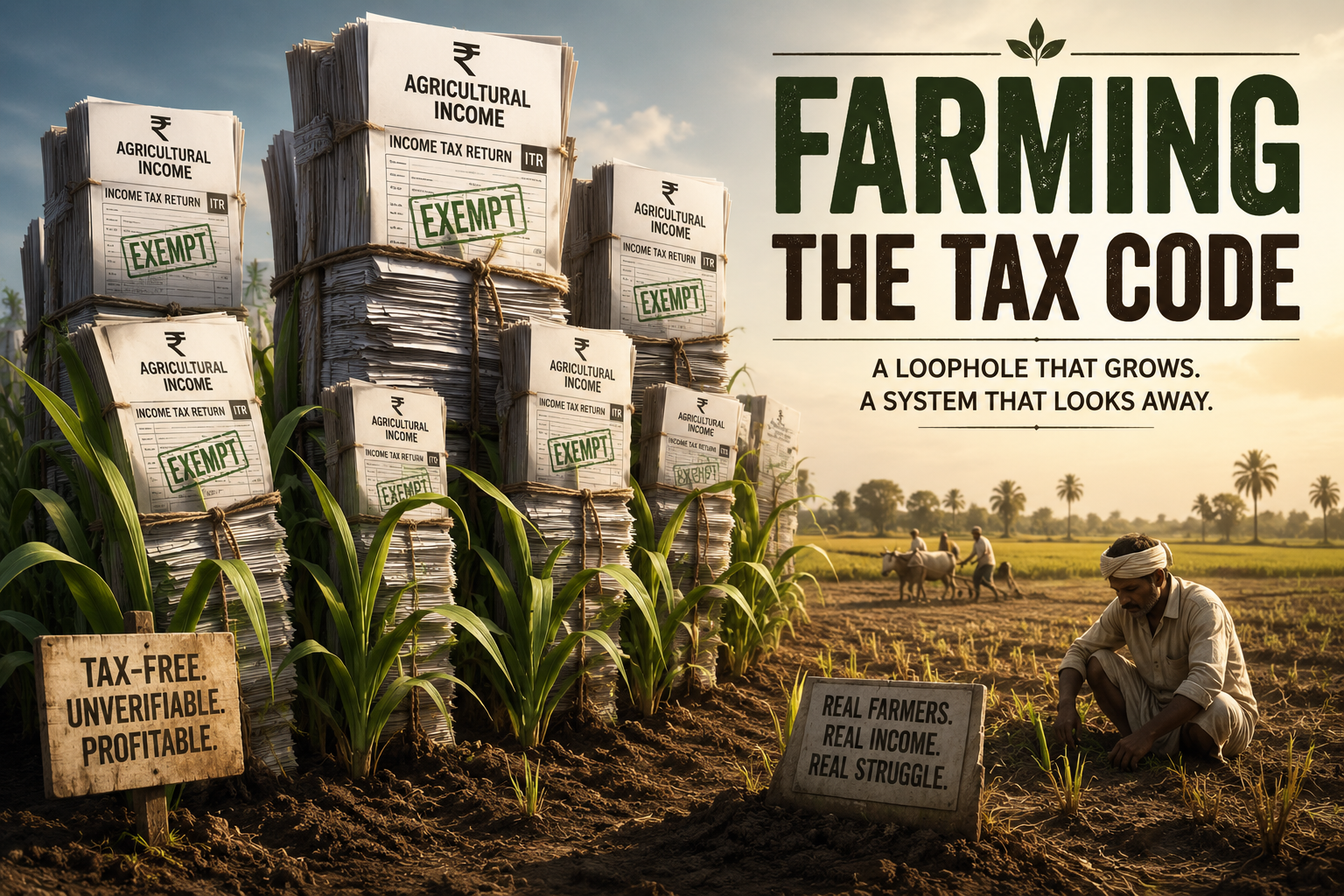

Agricultural Income: India's Most Abused Tax Loophole

By A Special Correspondent

First publised on 2026-06-21 10:48:30

About the Author

The Central Board of Direct Taxes has merely put numbers to a problem India has lived with for decades. In 310 detected cases alone, exemptions claimed total Rs 2,038 crore. These are not farmers. They are fraudsters wearing a farmer's mask.

The provision itself is not the problem. Section 10(1) of the Income Tax Act was designed to protect genuine cultivators - small landowners whose earnings are at the mercy of rain and soil. The intent was understandable. Agriculture in India has always been vulnerable to weather, fluctuating prices and uncertainty. But over time, that protection has been hollowed out. What remains is a loophole so expansive that developers, businessmen and political operators have converted it into a parallel financial highway.

The CBDT found cases involving individuals claiming enormous agricultural income despite lacking identifiable ownership or cultivation links to agricultural land. Some claims reportedly ranged from Rs 2 crore to Rs 50 crore. In other instances, commercial transactions involving agricultural land appeared to have been structured in ways designed to obtain agricultural tax treatment. The transaction may have been commercial; the tax outcome often looked agricultural.

The tax department had to look at fields from space to determine whether fields were even being cultivated. That detail deserves attention. India's tax administration is using satellite imagery because a self-reporting system without adequate verification becomes vulnerable to organised dishonesty.

The data covers assessment years 2020-21 through 2023-24. Four years of documented abuse. The issue is no longer whether the abuse existed. The real question is why the framework enabling it remains largely untouched.

The answer is politics - plain and simple.

Under Entry 82 of the Union List, Parliament's power to tax income excludes agricultural income, leaving states with the authority to tax it. While some states have historically imposed agricultural income taxes on specific plantation or commercial crops such as tea, broad-based taxation of agricultural income has largely remained absent. Any government that attempts to revisit the wider framework - even by introducing additional scrutiny above a prescribed threshold - risks being immediately branded anti-farmer. In a country where farm distress remains a permanent political flashpoint, that label carries serious electoral costs.

So the law stays - not because it genuinely protects farmers, but because the politics around it protects everyone else. The provision was originally designed with small cultivators in mind, but its largest practical advantages increasingly appear elsewhere. The most substantial gains from the exemption tend to accrue to those reporting very large agricultural incomes and, among them, some of the most aggressive claims appear disconnected from visible agricultural activity.

Every major political party understands this reality. Yet none appears eager to act. The farmer vote bank provides cover. The wealthy beneficiaries provide something else.

It is not a coincidence that agricultural income has frequently surfaced in discussions around opaque political funding and unexplained wealth. Unverifiable, tax-free and legally clean on paper, agricultural income offers an attractive route. Cash economies around land transactions, inflated farm income declarations and imaginative accounting around crop yields have long served as methods for moving money that cannot easily be explained. Political systems that benefit from opacity rarely show enthusiasm for dismantling it.

The CBDT's exercise is useful. Satellite mapping, data analytics and cross-referencing with land records are necessary tools. But enforcement against 310 cases, however vigorous, does not address the structural problem. The incentive remains intact: misclassify income as agricultural and obtain substantial tax advantages.

What is needed is a two-tier response - one that can be implemented administratively and another that requires legislative will.

The first tier is an annexure mandate. Any taxpayer claiming agricultural income above a prescribed threshold should file a detailed disclosure alongside the main return: survey numbers and documents establishing ownership or cultivation rights, crop-wise and season-wise yield details, and acreage under cultivation. Manufacturing units cannot claim production-linked benefits without disclosing factories, machinery and output. Large agricultural income claims should not be exempt from comparable scrutiny. Such requirements would spare small and marginal farmers from additional paperwork and place the burden exactly where abuse appears concentrated.

The second tier is a dedicated agricultural income return filed alongside the main ITR. A separate filing would compel claimants to provide information a general return does not seek - land records, acreage, yield declarations and state agriculture department linkages. More importantly, it creates a paper trail, something the present system conspicuously lacks. Patterns of abuse become harder to hide.

Neither measure harms a genuine farmer. Both measures dismantle the cover available to those who have never farmed a day in their lives.

That is precisely why neither will be easily adopted. The CBDT has supplied evidence for what had long survived as whispered truth and public suspicion. The farm was always a fiction. The tax saving was always the point.

The political class has perfected a familiar method: invoke the poor, protect the powerful. Agricultural income exemption may have been created for the farmer in the field. Today, too often, it serves the man whose closest encounter with farming is a tax return.

The lead image is AI-generated