The Loan Came With Strings. The RBI Has Finally Cut Them.

Editor-in-Chief of indiacommentary.com. Current Affairs analyst and political commentator. Author of Cyber Scams in India, Digital Arrest, The Money Trap and The Human Hack

View all posts by this Author

Editor-in-Chief of indiacommentary.com. Current Affairs analyst and political commentator. Author of Cyber Scams in India, Digital Arrest, The Money Trap and The Human Hack

View all posts by this Author

By Sunil Garodia

First publised on 2026-06-16 07:54:28

About the Author

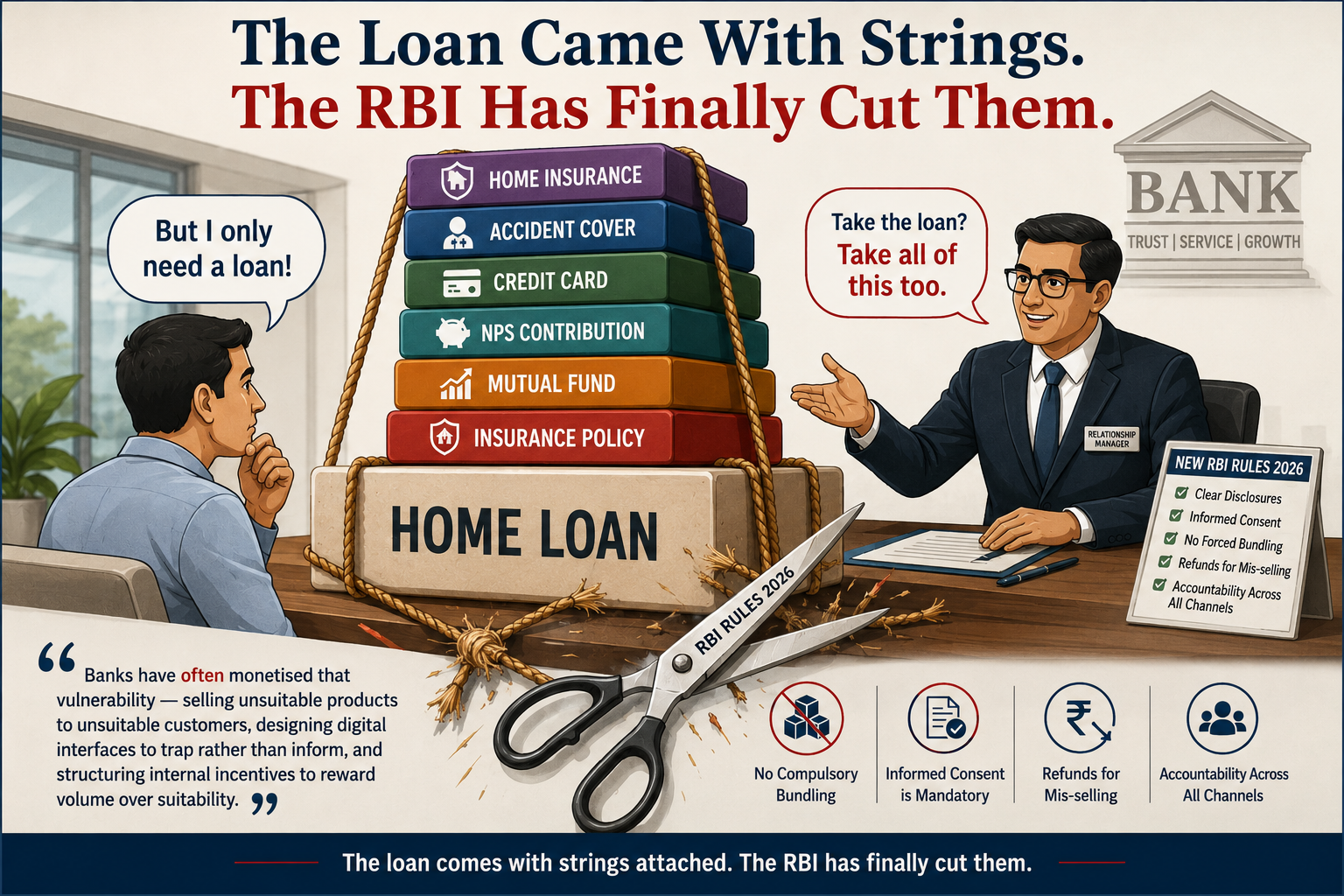

You walk into a bank seeking a home loan. You leave with a loan, an insurance policy you never requested, a credit card you never intended to obtain, and deductions you barely understood. Welcome to modern banking in India.

The Reserve Bank of India has finally acted to curb the practice.On June 15, 2026, the RBI issued rules to curb mis-selling of financial products by lenders, banning deceptive marketing tactics and tightening norms around customer consent, disclosures and sales practices. The rules, amendments to the RBI's Responsible Business Conduct Directions, will come into effect from January 1, 2027. India's borrowers have waited long enough for this moment.

The Problem Called Bundling

Banks have perfected the art of the captive sale. A borrower in need is a borrower in distress. Lenders know this.

Purchasing of term insurance, property insurance, and other policies is routinely presented as a precondition for sanctioning a loan. Borrowers feel they have no choice but to buy. In many reported instances, they are sold policies that bear no relation to their actual risk profile. Consider a retired schoolteacher taking a gold loan against her jewellery being sold a unit-linked insurance plan she will never need. Or a young salaried employee seeking a personal loan being bundled a credit life cover that, in the event of his death, pays the bank - not his family.

Bank relationship managers frequently market insurance products as high-return fixed deposits, sometimes misrepresenting them as short-term investments. The senior citizen who comes in to renew an FD goes home having signed an endowment policy. The signature was obtained. Informed consent was not.

The numbers expose the scale of the problem. Complaints under the RBI's Integrated Ombudsman Scheme rose 33% in FY24 and a further 13.5% in FY25, reaching 13.34 lakh. Loans and advances remained the single largest complaint category. Credit card grievances surged 20% in FY25 alone. In a telling first, complaints against private banks exceeded those against public sector banks. Behind every statistic is a customer who felt cheated and had nowhere else to turn.

Dark Patterns: Deception by Design

The mis-selling has moved online. Banks and NBFCs now deploy what technologists call "dark patterns" - digital interface designs engineered to manipulate rather than inform.

Examples include falsely implying urgency or scarcity to push a user into an immediate purchase, or offering pre-approved loans at attractive rates while warning that the rate will rise if the offer is not grabbed immediately. Buttons that accept are large and prominent. Buttons that decline are small and buried. The pre-ticked checkbox for insurance is not a UI oversight. It is a design choice.

The revised RBI provisions adopt a principle-based and channel-agnostic approach that also covers social media influencers and digital marketing intermediaries engaged by banks and financial institutions. The bank's liability does not end at its own website. The agent who mis-sold is the bank's agent.

Incentive Structures Drive Malpractice

This problem does not arise from individual moral failure alone. It is structurally engineered.

Branch managers operate under product-pushing targets. Relationship managers are evaluated - and paid - not merely on deposits mobilised or loans disbursed, but on third-party products sold. Insurance commissions in the bancassurance channel are among the highest in the industry. The incentive to mis-sell is not incidental to the system. It is baked into it.

The RBI has now directed that banks and NBFCs must ensure their policies and practices do not create incentives for mis-selling or lead to bundling of products and services. The regulator has recognised that the problem is systemic, not individual. That is a significant acknowledgement.

What the New Rules Say

The RBI's intervention is comprehensive. Lenders must now prominently disclose the key features of every product - including fees, charges, interest rates, risks, financial commitment, lock-in conditions, and exit terms including penalties - in a manner that draws the customer's attention to such material information.

Banks must obtain clear and informed consent before selling any product. The consent must be recorded and cannot be assumed or pre-selected. Under the new rules, a pre-ticked box does not constitute consent, and a signature obtained under pressure is not treated as genuine agreement.

Banks shall not resort to compulsory bundling of any third-party product or service with any of their own products or services. This is a categorical prohibition, not a guideline.

In cases where mis-selling is established, the bank shall refund the entire amount and inform the customer about cancellation of the sale. Banks must also compensate for any consequential loss. Customers will have a 30-day feedback window, and banks must conduct half-yearly reviews of grievances to implement improvements.

Will Banks Comply?

Scepticism is warranted. The RBI has expressed concern about mis-selling since at least 2015. As recently as July 2025, RBI Deputy Governor M Rajeshwar Rao publicly criticised banks for forcing products on customers, particularly the elderly. The warnings produced little institutional change. Complaints kept rising.

What is different this time is the combination of a categorical definition of mis-selling, mandatory refunds, and channel-agnostic accountability. Claiming the customer signed a form will no longer be sufficient defence. Even if a customer signed, the regulator has made clear that this does not automatically constitute genuine consent. Whether banks change behaviour before January 1, 2027, or wait to be caught and forced to refund remains to be seen.

The Consumer Must Also Act

Regulation is necessary. It is not sufficient. Borrowers must ask one question at every loan counter: is this product mandatory for my loan, or is it being bundled? If it is bundled, they should refuse it and ask for the refusal to be noted in writing. If they have already been mis-sold a product, the new rules give them the right to complain and demand a full refund. The RBI Ombudsman portal is available at cms.rbi.org.in. The relationship manager at the bank counter is not your financial advisor. He is a salesperson with a target.

Conclusion

Indian banking has operated for decades on the assumption that a borrower in need will accept whatever is placed before him. Banks have often monetised that vulnerability - selling unsuitable products to unsuitable customers, designing digital interfaces to trap rather than inform, and structuring internal incentives to reward volume over suitability.

The RBI has now drawn a line. The burden on the consumer will reduce. The burden on the bank to prove informed consent will increase. Full refunds for mis-selling will make it expensive to exploit. Apart from being good regulation, that is the beginning of honest banking.

The lead picture is AI-generated